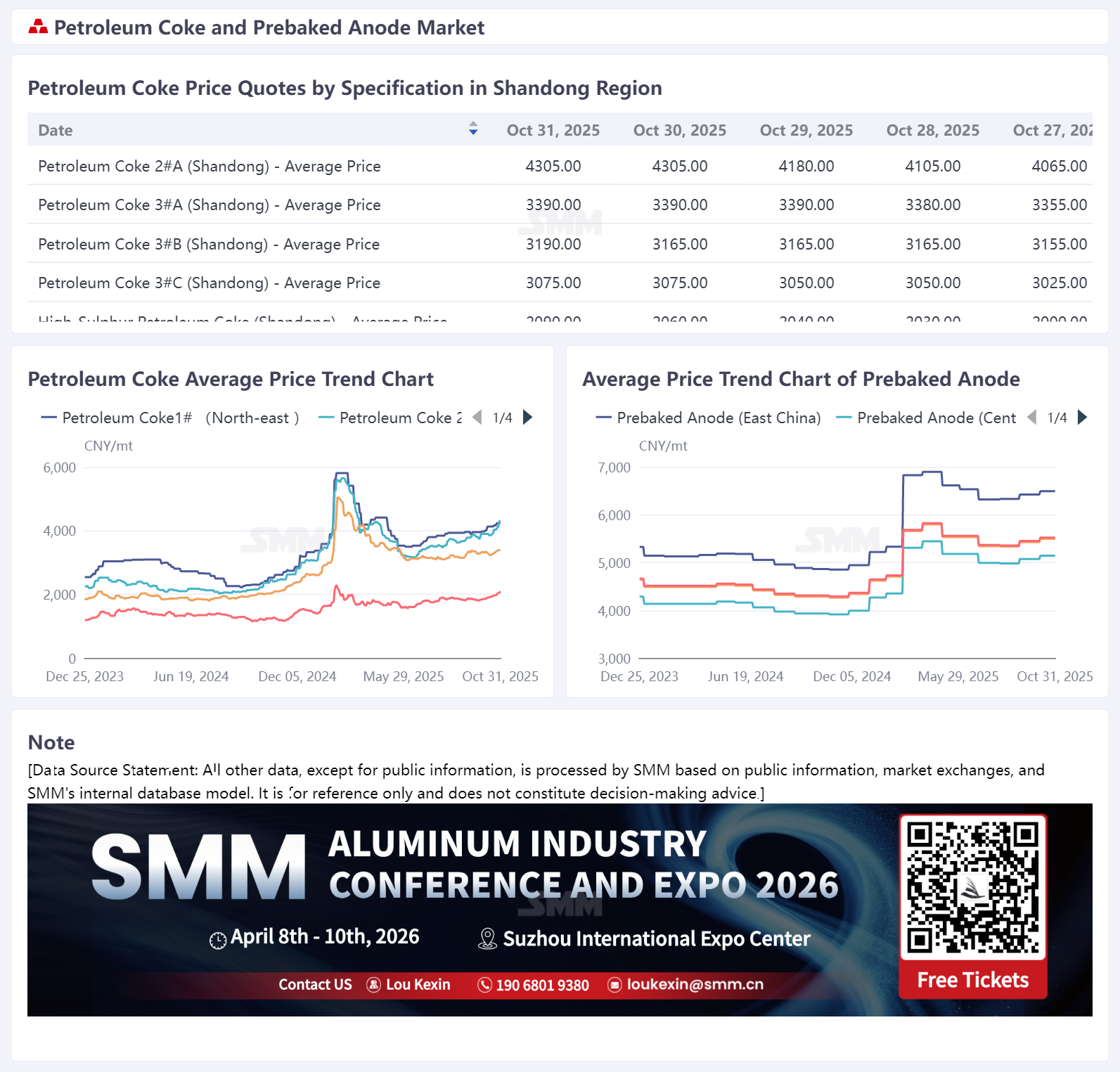

Pada bulan Oktober, harga anoda pra‐panggang SMM terus mengalami tren naik。 Harga patokan pengadaan untuk pabrik aluminium di Shandong pada Oktober 2025 adalah 4,902 yuan/ton, naik 1,45% dibandingkan bulan sebelumnya。 Menurut SMM, harga pesanan ekspor anoda pra‐panggang terutama meningkat pada Oktober, dengan penyesuaian terkonsentrasi pada kisaran $10‐20/ton。 Hingga saat ini, harga anoda SMM di China timur ditutup pada 4,902‐8,087 yuan/ton。

Di pasar bahan baku, kokas minyak bumi dan tar batubara menunjukkan tren yang berbeda。 Di pasar kokas minyak bumi, kokas minyak bumi belerang‐rendah menunjukkan kinerja yang sangat baik: didorong oleh pembelian aktif dari pasar bahan anoda, pengiriman kilang tetap umumnya sehat; yang lebih penting, produksi kokas minyak bumi di beberapa kilang di China timur‐laut menurun, menyebabkan ekspektasi pasar terhadap pengetatan pasokan。 Dengan beberapa faktor positif digabungkan, harga kokas minyak bumi belerang‐rendah terus naik。 Menurut statistik SMM, hingga saat ini, harga rata‐rata kokas minyak bumi belerang‐rendah di China timur‐laut adalah sekitar 4,204 yuan/ton, naik 3,62% dari 30 September, dengan kenaikan lebih lanjut diperkirakan pada awal November。 Karena antusiasme pembelian yang kuat dari karbon hilir yang digunakan dalam produksi aluminium dan perusahaan bahan anoda, dukungan sisi permintaan tetap kuat。 Kilang‐kilang besar menaikkan harga kokas minyak bumi beberapa kali, sementara harga kilang lokal juga menguat。 Data menunjukkan bahwa, hingga saat ini, harga rata‐rata SMM untuk kokas minyak bumi dari kilang lokal adalah 2,918 yuan/ton, naik sekitar 14,22% dari 30 September。 Di pasar tar batubara, harga tar batubara bahan baku turun selama bulan tersebut, menyebabkan dukungan sisi biaya lebih longgar, dan harga tar batubara terutama menurun。 Menurut data SMM, hingga saat ini, harga rata‐rata tar batubara adalah 3,747 yuan/ton, turun 3,60% dari 30 September。 Secara keseluruhan, kenaikan tajam dalam kokas minyak bumi memberikan dukungan yang solid untuk biaya anoda pra‐panggang。

Sisi pasokan, perusahaan anoda pra‐panggang menunjukkan pola beragam peningkatan dan pemotongan produksi bulan ini。 Proyek baru di Yunnan, Guangxi, Mongolia Dalam, Hunan, dan wilayah lainnya baru‐baru ini mulai beroperasi satu per satu, membawa peningkatan pasokan yang jelas ke pasar。 Sementara itu, beberapa perusahaan di Henan menghadapi kendala produksi karena kontrol terkait lingkungan, perusahaan individu di China barat‐laut melihat penurunan output karena faktor lingkungan, dan beberapa perusahaan di wilayah lain mengalami penarikan produksi karena masalah peralatan atau pemeliharaan。 Secara keseluruhan, output yang dirilis dari startup proyek baru memberikan dukungan utama, dan pasokan anoda pra‐panggang domestik meningkat dibandingkan dengan periode sebelumnya。

Di sisi permintaan, kapasitas operasi aluminium domestik terus tetap tinggi. Memasuki November 2025, pembatasan lingkungan hidup musim dingin diperkirakan akan memengaruhi tingkat operasi perusahaan-perusahaan tertentu. Namun, mengingat bahwa produksi aluminium tidak bisa langsung turun menjadi nol segera setelah penutupan jalur produksi, perubahan produksi diperkirakan akan relatif kecil. Permintaan domestik untuk anoda prabakar tetap menguntungkan. Mengenai pesanan ekspor, berdasarkan data ekspor anoda prabakar September 2025, ekspor anoda prabakar Tiongkok mencapai 206.300 metrik ton, naik 11,90% YoY tetapi turun 1,06% MoM, menunjukkan fluktuasi yang relatif kecil dari bulan sebelumnya. Ekspor kumulatif anoda prabakar untuk tahun 2025 mencapai 1,6445 juta metrik ton, naik 4,10% YoY. Secara khusus, pesanan yang diekspor ke Kanada, UEA, Indonesia, dan Jerman menunjukkan peningkatan yang signifikan, dengan kenaikan masing-masing melebihi 10.000 metrik ton, dengan total lebih dari 57.600 metrik ton. Sebaliknya, pesanan ke Malaysia, Spanyol, Islandia, dan Arab Saudi mengalami penurunan yang substansial, dengan penurunan masing-masing melebihi 9.000 metrik ton, dengan total sekitar 48.100 metrik ton. Di sisi harga, harga ekspor anoda prabakar meningkat pada September, dengan harga ekspor rata-rata naik 19,40% YoY. Didukung oleh kenaikan biaya bahan baku domestik, harga ekspor anoda prabakar terus mengalami tren kenaikan pada Oktober. Secara keseluruhan, pesanan ekspor anoda prabakar saat ini menunjukkan daya tahan yang cukup, dan tren kenaikan harga tetap solid.

Komentar Singkat: Sejauh ini, sebuah perusahaan aluminium di Shandong telah mengumumkan harga acuan tender anoda prabakar November 2025, yang naik 222 yuan/metrik ton MoM. Secara bersamaan, sebuah perusahaan penjualan anoda prabakar domestik utama menaikkan harga penjualannya sebesar 251 yuan/metrik ton MoM. Menurut data SMM, per 31 Oktober, biaya komprehensif Tiongkok untuk anoda prabakar meningkat menjadi 5.125 yuan/metrik ton, naik 3,31% dari 30 September. Pasar bahan baku saat ini berkinerja baik, memberikan beberapa dukungan untuk harga anoda prabakar. Khususnya untuk kokas minyak, permintaan hilir umumnya menguntungkan, antusiasme pembelian di industri karbon sedang, dan permintaan dari pasar bahan anoda untuk kokas minyak terus berlanjut. Mempertimbangkan berbagai faktor, pusat harga kokas minyak pada November diperkirakan akan naik. Dalam latar belakang ini, harga anoda prabakar, yang secara langsung didukung oleh kenaikan biaya bahan baku, diperkirakan akan terus mengalami tren kenaikan.